Having A Hard Time Recognizing House Mortgages? Comply With These Tips!

Written by-Silva SpiveyMortgages are important when it comes to owning or buying your home, but a lot of people aren't sure of what to do and spend too much when they're getting a mortgage. The tips you see here give you information about making your mortgage optimal. Keep reading for more information.

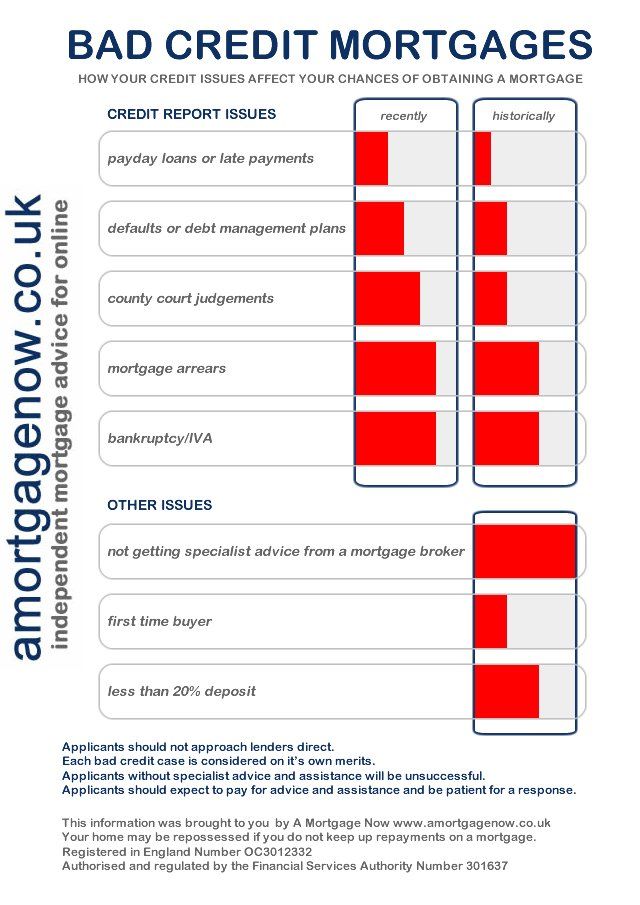

There are loans available for first time home buyers. These loans usually do not require a lot of money down and often have lower interest rates than standard mortgages. Most first time home buyer loans are guaranteed by the government; thus, there is more paperwork needed than standard mortgage applications.

Before applying for a mortgage, pay down your debts. Lenders use a debt to income ratio to verify that you are able to afford a mortgage. A general rule of thumb is 36 percent of your gross income should be available to pay all of your monthly expenses, including your mortgage payment.

Prepare your paperwork before applying for a mortgage. There are many items that a lender will require. These items include the last two or three years worth of tax returns, copies of each of your monthly credit card statements and installment loans. Three months bank statements and two months worth of pay stubs are also needed for approval.

Before you refinance your mortgage, make sure you've got a good reason to do so. Lenders are scrutinizing applications more closely than ever, and if they don't like the reasons you're looking for more money, they may decline your request. Be sure you can accommodate the terms of the new mortgage, and be sure you look responsible with the motivations for the loan.

When you decide to apply for a mortgage, make sure you shop around. Before deciding on the best option for you, get estimates from three different mortgage brokers and banks. Although, interest rates are important, there are other things you should consider also such as closing costs, points and types of loans.

If you are offered a loan with a low rate, lock in the rate. Your loan may take 30 to 60 days to approve. If you lock in the rate, that will guarantee that the rate you end up with is at least that low. Then you would not end up with a higher rate at the end.

Try giving your lender a chance to help you with mortgage payment problems. If you struggle to make payments, do not ignore your lender's services. There are various new programs to help you keep up with your mortgage payments like forbearance if you have an FHA mortgage. Lenders are generally happy to work out any delinquent loans via loan modifications, or possibly short sales if you can't afford to keep your home. It can be difficult to deal with them over this, but communication is key.

Pay off or lower the amount owed on your credit cards before applying for a home mortgage. Although your credit card balances do not have to be zero, you should have no more than 50 percent of the available credit charged on each credit card. This shows lenders that you are a wise credit user.

Know your credit score and verify its accuracy. Identity theft is a common occurrence so go over your credit report carefully. Notify the agency of any inaccuracies immediately. Be particularly careful to verify the information regarding your credit limits. Make all your payments in a timely manner to improve your score.

In order to get the best mortgage rate, keep a high credit score. You can order a credit report from the top three reporting agencies. Check the report for errors. As a general rule, many banks stay away from credit scores below 620 nowadays.

You can request for the seller to pay for certain closing costs. For example, a seller can pay either a percentage of the closing cost or for certain services. Many times the seller is responsible for paying for a termite inspection along with a survey and appraisal of the property.

Most financial institutions require that the property taxes and insurance payments be escrowed. This means the extra amount is added onto your monthly mortgage payment and the payments are made by the institution when they are due. This is convenient, but you also give up any interest you could have collected on the money during the year.

Be careful about quicksand mortgages. These are mortgages that have all sorts of hidden tricks in them like balloon payments, prepayment penalties, tons of upfront fees, and more. These loans typically are only helpful to the lender, not to the customer. In fact, they can make your loan down right unaffordable over time.

Be sure to explore all financing and refinancing options with your mortgage broker. You may be able to refinance your home mortgage without closing costs. When this is the case, you will pay a little more in monthly payments; however, in the long run you could save a great deal of money.

Talk to the BBB before making your final decision. Deceitful brokers may con you into paying high fees and refinancing so that they can make more money. If a broker wants you to pay excessive points or high fees, be cautious.

You should have the proper paperwork ready in advance for a lender. Look well prepared. You'll need a copy of your pay stubs going back at least two paychecks, your last year's W-2 forms and a copy of last year's tax return. You'll also need your bank statements. Get those together before the lender asks.

If you have less than perfect credit, one way to overcome it is to have a large down payment, more than most other borrowers. It is common for people to save between three and five percent, but you should aim for around twenty if you want to increase your chances of being approved.

With the valuable advice that has been discussed in this article, you're ready to jump out there and get going. The right mortgage is just around the corner. All you have to do is evaluate what is best for you with the criteria given. You will find yourself in a mortgage that makes you feel protected.